by David Williamson

If you read this blog, then you're probably familiar with Ronald Coase's work on the importance of transaction costs. But did you know that Coase devoted a substantial portion of his early career to criticizing the Cobweb Model? He actually wrote 4 separate articles on the subject between 1935 and 1940, but not one makes Dylan Matthew's list of Coase's top-five papers. This work is actually really fascinating in the context of economic intellectual history, so here is a quick summary!

The 1932 UK Reorganization Commission for Pigs and Pig Products Report

It all started when the UK Reorganization Commission for Pigs and Pig Products claimed in a 1932 report that government intervention was needed to stabilize prices in the hog industry. The Commission found that hog prices followed a 4-year cycle: two years rising and two years falling. The Commission explained this cyclical behavior using the Cobweb Model. In this model, products take time to produce. So, to know how much to produce, firms have to guess what the price will be when their product is ready to bring to the market. If producers are systematically mistaken about what prices will be, this could lead to predictable cycles in product spot prices.

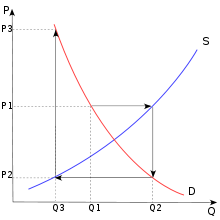

The Cobweb Model

How forecasting errors can lead to cycles in product prices is illustrated in the figure below. Suppose we begin time at period 1 and hog producers bring Q1 to the market to sell. Supply is essentially fixed this period because producers can't produce more hogs on the spot, so the price that prevails on the market will be P1. Since this price exceeds the marginal cost of production (represented by S), the individual producers wish they had produced more. Now, when the producers go back home to produce more hogs, they have to guess that the price will be when their hogs are ready to sell. Suppose it will take 2 years to produce more hogs. The UK Reorganization Commission argued that hog producers will assume the price of hogs next period will be the same as it was this period (in other words that producers had "static" expectations about price). That means, in this context, hog producers think the price of hogs in 2 years will still be P1. So each producer will individually increase production accordingly. However, when the producers return to the market in 2 years, they will find that everyone else increased production too and that quantity supplied is now Q2. As a result, the price plummets to P2 and the producers actually lose money. Not learning their lesson, the hog producers will again go home and assume that the price next period will be P2 and collectively cut back their production to Q3. Hopefully you see where this is going, even if the hog producers don't. The price will go up again in 2 years and then down again in 2 more. Thus, we have a 4-year cycle in hog prices. How long will this cycle continue? That depends on the elasticities of supply and demand. If demand is less elastic than supply, as was believed to be the case in the hog market, then the price swings will continue forever and only get bigger as time goes on.

Source: Wikipedia

Coase Takes the Model to the Data

The Cobweb Model is really clever, but does it actually capture the reality of the hog market? Coase and his co-author Ronald Fowler tried to answer that question by evaluating the model's assumptions. First, are hog producer expectations truly static? Expectations cannot be observed directly, but Coase and Fowler (1935) used market prices to try and infer whether producer expectations were static. It didn't seem like they were. Second, does it really take 2 years for hog producers to respond to higher prices? Coase and Fowler (1935) spend a lot time discussing how hogs are actually produced. They found that the average age of a hog at slaughter is eight months and that the period of gestation is four months. So a producer could respond to unexpectedly higher hog prices in 12 months (possibly even sooner since there were short-run changes producers could also make to increase production). So why does it take 24 months for prices to complete their descent? Even if we assumed producers have static expectations, shouldn't we expect the hog cycle to be 2 years instead of 4?

This evidence is hard to square with the Cobweb Model employed by Reorganization Commission, but Coase's critics were not convinced. After all, if it wasn't forecasting errors that were driving the Hog Cycle, then what was? "They have, in effect, tried to overthrow the existing explanation without putting anything in its place" wrote Cohen and Barker (1935). Coase and Fowler (1937) attempted to provide an explanation, but this question would continue to be debated for decades.

The Next Chapter

Ultimately, John Muth (1961) proposed a model that assumed producers did not have systematically biased expectations about future prices (in other words that they had "rational" expectations). Muth argued this model yielded implications that were more consistent with the empirical results found by Coase and others. For example, rational expectations models generated cycles that lasted longer than models that assumed static or adaptive expectations. So a 4-year hog cycle no longer seemed as much of a mystery. I'm not sure what happened to rational expectations after that. I hear they use it in Macro a bit. Anyways, if you are interested in a more detailed summary of Coase's work on the Hog Cycle, then check out Evans and Guesnerie (2016). I found this article on Google while I was preparing this post and it looks very good.

References

Evans, George W., and Roger Guesnerie. "Revisiting Coase on anticipations and the cobweb model." The Elgar Companion to Ronald H. Coase (2016): 51.

Coase, Ronald H., and Ronald F. Fowler. "Bacon production and the pig-cycle in Great Britain." Economica 2, no. 6 (1935): 142-167.

Coase, Ronald H., and Ronald F. Fowler. "The pig-cycle in Great Britain: an explanation." Economica 4, no. 13 (1937): 55-82.

Cohen, Ruth, and J. D. Barker. "The pig cycle: a reply." Economica 2, no. 8 (1935): 408-422

Muth, John F. "Rational expectations and the theory of price movements."Econometrica: Journal of the Econometric Society (1961): 315-335.